Summary

- Elon Musk warns of necessary “breaking” and temporary hardship to fix economic issues, suggesting potential stock market pain followed by a strong recovery.

- We analyse current economic factors using the GDP formula, noting declining consumer sentiment, uncertain business investment, reduced government spending, and complex trade dynamics due to tariffs.

- I have turned from Neutral to a Bearish outlook for 2025, citing liquidity risks, a significant debt refinancing challenge, and potential negative impacts from trade wars.

- I am taking a cautious investment approach, having raised cash levels to 50%, written covered calls, and implemented small hedges, while anticipating buying opportunities during the next market correction or bear market.

Elon Musk has warned that in order to fix things, we need to break them first. He has agreed that the stock market would suffer pain during the breaking phase. I believe him.

He also suggested that the pain was necessary and that the fixes would lead to a strong recovery after. I sure hope so.

Here are some thoughts on DOGE, tariffs, macro, and markets. Take it for what it’s worth, but remember, I warned about a bear market in 2022 at the end of 2021, said to expect a huge up year in 2024, and warned about volatility in 2025. I get things right sometimes.

Musk Says, “Brace For Hardship”

In the week leading up to the election, a torrent of thoughts came from Musk and his wider circle. Most of them had to do with the idea that the government was fat, corrupt, and needed massive pruning.

Musk, of course, volunteered to do the pruning via DOGE, the Department Of Government Efficiency, which of course, and I think planned long in advance, has the same name as Musk’s pet crypto.

During a town hall meeting on Oct. 25, Musk said DOGE would “necessarily involve some temporary hardship.” He went on to agree with this post on X.com after the town hall…

I have been thinking about those statements and posts since they were made. They largely went into my reasoning for why 2025 would be a volatile year.

The Short-Term Economics Are Negative

A lot of President Trump’s voters continue to cheerlead, and until very recently promote bullish economic and market narratives. Many of the bullish narratives are still out there, some from the cheerleaders, others from people I simply disagree with.

For me, my analysis attempts to rise above politics and rationalization of belief. If 37 years of study and experience have taught me anything, it’s that popular narratives are often wrong, misused or, mostly, incomplete.

Here’s the economic reality as I see it. It’s fairly straightforward as if I pulled out my Econ 301 Micro and Econ 302 Macro textbooks again.

The formula for GDP is: GDP = C + I + G + (X-M), where C represents consumer spending, I is investment, G is government spending, and (X – M) represents net exports (exports minus imports).

Let’s break that down a bit.

Consumer spending is largely led by consumer sentiment.

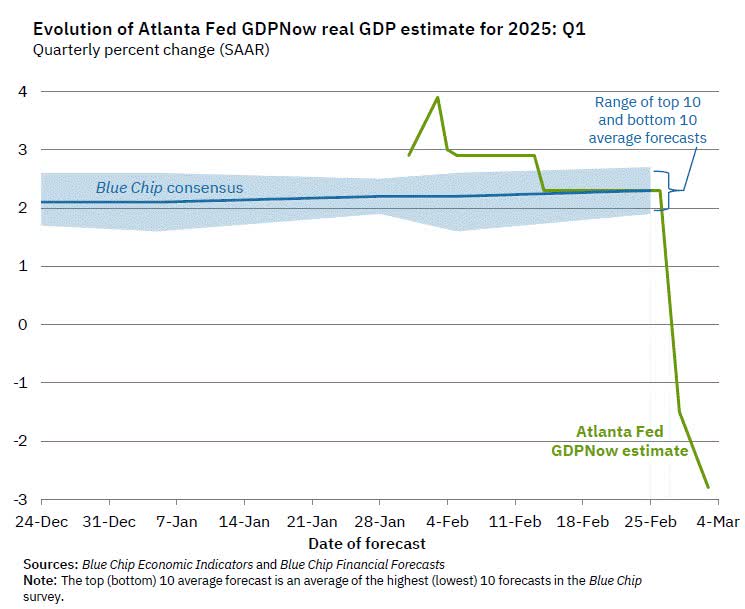

The University of Michigan Consumer Sentiment Index fell sharply to 64.7 in February, down from 71.1 in January. This is the lowest level since November 2023 and represents a 9.76% decrease from the previous month. In addition, the Conference Board Consumer Confidence Index dropped 7.0 points to 98.3 in February, marking the largest monthly decline since August 2021.

The quick impact on the economy is suddenly appearing.

GDPNow (Atlanta Federal Reserve)

Investment by businesses into the economy is uncertain right now. Certainly, there have been a few big headlines from companies like Taiwan Semiconductor Manufacturing Company Limited (TSM), Apple Inc. (AAPL) and others about new U.S. investments. However, those will take time to play out.

In January, Deloitte forecast that uncertainty would continue to hamper investment. On the flip side, according to the JPMorgan U.S. Business Leaders Outlook for 2025, optimism is rebounding.

I’m going to call investment items a flip that we will have to watch in the coming months. I’m optimistic that strong corporate balance sheets will spur investment in domestic supply chains, but that will take time. We’ll see if any shocks thwart business investment.

Government spending is clearly coming down, even if not quite consistent with some claims from DOGE. If government spending is cut 5-10% as Musk claims, then that’s a drag on the economy in the short term, but also a reduction in ongoing deficit spending.

So, in the short term, government spending comes down, leading to some economic pressure short term, but, the reduction in deficit spending could help mitigate the burgeoning debt.

Exports minus imports in this new tariff age is where things get very interesting. We have to not only think about the immediate trade impacts of tariffs, but also consider all of the above economic factors in relation to the trade war. There are a lot of moving parts.

In general, economic theory posits that tariffs lead to inflation and imbalances. I think we have seen that historically, including near the Great Depression when tariffs were not used selectively to target cheaters and dumpers.

The risk that President Donald Trump runs, especially in how it deals with Canada and Mexico, is that supply chains suffer serious damage that takes years to fix domestically. Count me as one who thinks the tariffs on Canada and Mexico are ill-advised.

I’m not so pessimistic about China tariffs economically. China has been cheating for decades by subsidizing industries, such as steel, and “dumping” products on global markets. Dumping has the real impact of harming competitors, and in some cases comes with national security concerns.

Exports would be expected to decline due to retaliatory tariffs by trade partners, as we have seen from Canada and China.

Imports will likely also decline as certain products become less cost advantageous. The problem we likely see, in my opinion, is a lag in supply chain development in the U.S. for certain scarce goods and materials think Canadian crude, lumber, steel, and aluminum.

The net effect is impossible to calculate here, but, the odds of it being positive in the short term are almost zero from what I see.

So, that leaves us with a pretty bleak picture for 2025 economically. Will we get a recession? I don’t know, but a recession scare is currently underway.

The Stock Market In 2025

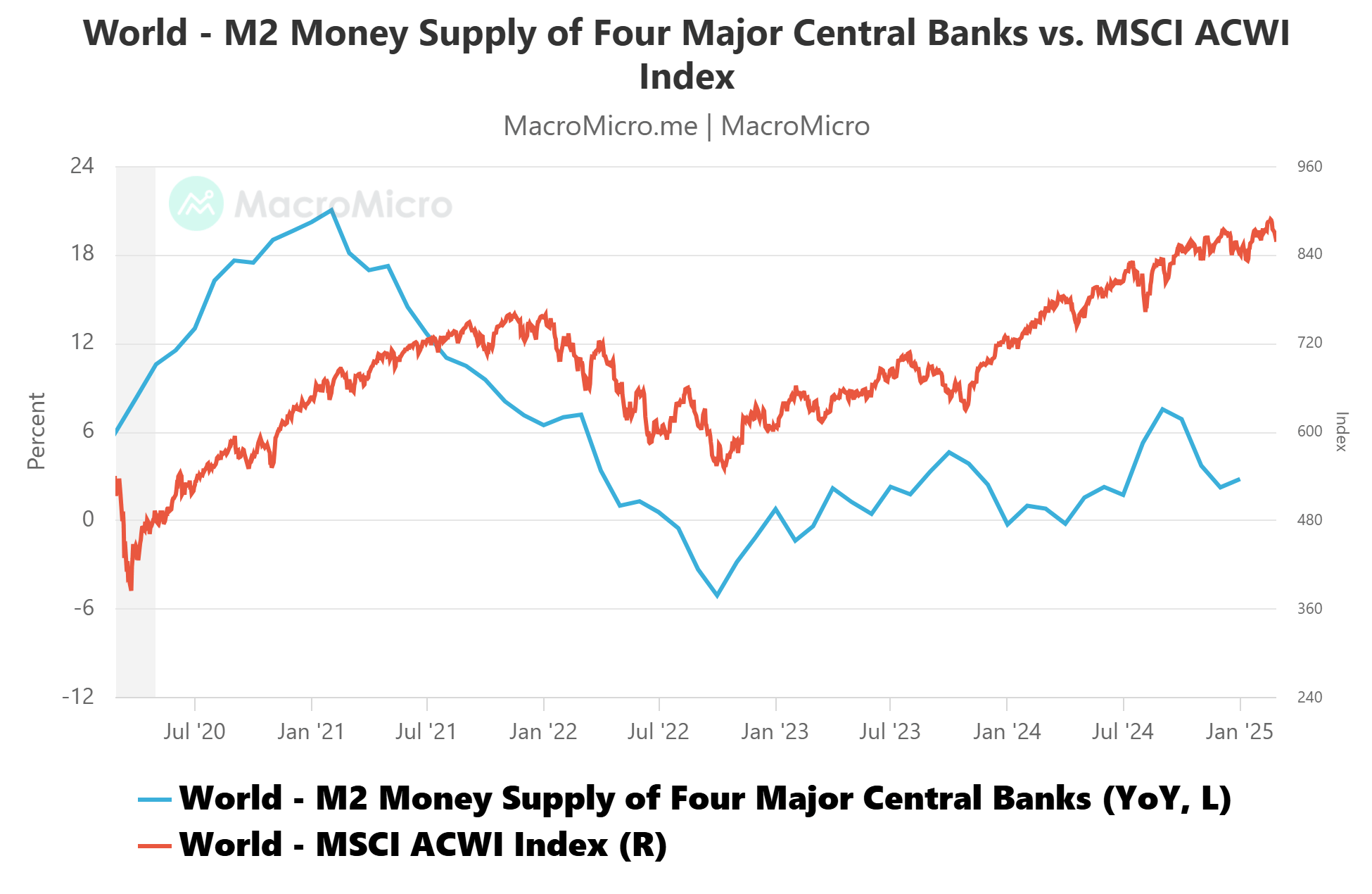

The stock market is very tied to global liquidity. I talked about that in a recent Investment Experts podcast.

Liquidity Up, Markets Up, Liquidity Down, Markets Down

In the economic current environment, M2 liquidity is at risk of turning down.

Not only do we have all the economic factors of GDP noted above, but we also face a $6.2 trillion debt wall to refinance in 2025-2026.

U.S. Treasury Secretary Scott Bessent in his first auction ran things essentially the same as Janet Yellen, but his stated goal is to get the 10-year U.S. Treasury rate down so he can write longer-term debt.

The risk on near-term debt is that the U.S. faces short-term crowding out that negatively impacts liquidity into next year. We’ll see, but I do not think there’s much chance to avoid at least some pressure from the debt refinancing.

So, GDP factors and debt refinancing appears to be net negative on liquidity, as is the trade war.

Here’s the correlation to make it easy to see.

M2 Money Supply & Markets (MacroMicro)

Apollo Global Management has done a lot of work on the relationships between liquidity and asset prices, as have others. What I’m saying here is not speculation. The correlation is very real.

If liquidity drops, then you should expect asset prices to drop.

I expect liquidity to drop. I could be wrong, but, my confidence level is about as high as it has ever been, and as noted above, my track record is pretty good.

Closing Investment Quick Thoughts

As you can read from my articles, I came into 2025 from neutral to bearish.

I’m no longer neutral.

I have raised my cash levels to 50%, written covered calls on a large portion of my remaining favorite equity, and have a few small hedges with puts bought on the SPDR® S&P 500® ETF Trust (SPY).

One of the lessons I have learned is that no matter how much we hurt the economy, it always comes back. Warren Buffett has talked about this for decades.

I do not know if this year will look more like 2018, 2022, or, gasp, 2008 yet. Heck, there might even be one last puff on the cigar and the correction I see doesn’t happen until later (in which case it will be bigger).

Regardless, I will be buying the next correction or bear market at some point. When I see the pivot coming, which will come when people throw in the towel, maybe not until year-end is my best guess, I will be a net buyer again.

Kirk Spano

Founder | Head of Investment Research and Analysis